We are excited to announce that Brink is now part of Africa Practice. Learn more

Africa: Trends to watch in 2026

As we approach the end of 2025, Africa Practice has considered the key trends to follow in 2026. We consider issues transcending geopolitics, climate, geoeconomics, elections, and security. We also revisit some of the predictions we made last year and forecast the key dynamics to watch in the year ahead.

Geopolitics

1. Summitry sees African agency peak and recede

Last year, Africa Practice warned that the re-election of Donald Trump as US president in November 2024 would usher in another era of American isolationism, accompanied by trade tariffs and cuts to funding for development and multilateral agencies.

Indeed, the magnitude of Trump’s punitive tariffs, unveiled on “Liberation Day” in April 2025, put global leaders on the back foot. By the time of the BRICS summit in July, it became apparent that governments were preoccupied with mitigating the impact of US tariffs, with Trump threatening additional 10% levy on BRICS members. Nevertheless, the summit in Rio de Janeiro, Brazil, marked a high-water mark for continental participation with South African President Cyril Ramaphosa, Ethiopian Prime Minister Abiy Ahmed, and Egyptian Prime Minister Mostafa Madbouly all in attendance, alongside partner state representatives, Nigerian President Bola Tinubu and Ugandan Vice-President Jessica Alupo. Alas, extra seats at the table led to disagreements over the wording of the summit communiqué, with African states divided over who should represent the continent on a reformed UN Security Council. By contrast, there was greater consensus among BRICS members that artificial intelligence (AI) governance required greater attention, with the BRICS Leaders’ Declaration acknowledging the need to mitigate potential risks and calling for the UN to lead in defining global standards. Tech is likely to remain high on the agenda in 2026, as India assumes the BRICS presidency.

The G20 summit in Johannesburg, South Africa, last month marked a second high-water mark, as this was the first to take place on the African continent. Regrettably, the US left a cloud over this gathering too, with Trump boycotting the summit, and his populist ally Argentine President Javier Milei chastising South Africa for proceeding to issue a statement in America’s absence. Despite such disruption, the G20 Leaders’ Declaration contained salient themes from South Africa’s year-long presidency, with global inequality and African development at the forefront of the agenda. Key outcomes included a commitment to triple renewable energy capacity by 2030, recognition of the need for urgent action to address loss and damage arising from climate change, and support for low- and middle-income countries to address their debt vulnerabilities, including through smarter implementation of the G20 Common Framework. While some of these measures lack concrete actions and accountability mechanisms, the South African Presidency nevertheless showcased an unwavering commitment to multilateralism amid considerable headwinds.

The outlook for 2026 is less rosy, with South Africa handing over leadership of the G20 to the USA. Regrettably, the American G20 Presidency is intent on ditching hard-won commitments to solidarity, equality and development, and pursuing an agenda focused on cutting red tape to boost economic growth, and promoting technology and innovation. Trump is also intent on punishing South Africa for its supposed persecution of its white minority. Officials in Pretoria are already bracing for the prospect of exclusion from the next G20 summit in mid-December 2026, which is due to take place at Trump’s private golf resort in Miami, Florida. We expect the year ahead to be dominated by friction between the US administration and other G20 members over who gets to decide the guest list for the gathering.

2. Heightened geopolitical rivalry creates opportunities for strategic actors

Last year, we predicted that America’s disdain for multilateralism could create opportunities to strengthen African agency. To some extent, heightened geoeconomic and geostrategic competition between the US and China has echoes of the Cold War, with intense rivalry between the superpowers creating opportunities for African states to play states off against each other and maximise benefits. Indeed, Trump’s inaugural Africa summit in July 2025 showed the ability of smaller African states to capitalise on interest from Washington and Beijing to punch above their weight, especially where energy, security and migration interests abound.

Senegalese President Bassirou Diomaye Faye was invited to Trump’s summit barely nine months after co-hosting the Forum on China-Africa Cooperation (FOCAC). While migration will have doubtless been on the agenda, Faye’s seat at the table can be partly explained by the importance of the Tortue LNG project to US firm Kosmos Energy, which discovered the field, and BP, which operates it. Both companies carry considerable weight in Washington, and will have leveraged the visit to strengthen ties with Faye and his Mauritanian counterpart Mohamed Ould Ghazouani during their time on Capitol Hill. BP and Kosmos likely used the summit to better understand Senegal’s plans to renegotiate oil, gas and mining contracts agreed under the previous regime, especially given Prime Minister Ousmane Sonko’s allegations of irregular payments to then-President Macky Sall’s brother Aliou. The visit will have also been beneficial for US policy-makers who regard Senegal as a bulwark against instability emanating from the Sahel, including the threat posed by Islamic terrorism, and the proximity of military regimes in Burkina Faso, Mali and Niger to Russia. The three juntas – which are increasingly aligned under the Alliance of Sahel States – have been particularly hostile to Western investors, including French and Canadian mining firms.

Gabonese President Brice Oligui Nguema was also among the African statesmen entertained by Trump, with mineral resources and maritime security also likely high on the agenda. General Oligui is best known for leading the coup d’état against Ali Bongo, bringing an abrupt end to a political dynasty that had been in power since 1967. Soon after seizing power, he promoted a greater role for Gabon’s national oil company, leveraging its pre-emption rights to acquire Assala Energy, a subsidiary of US investment firm Carlyle. The nationalisation boosted Oligui’s profile, enabling him to secure election as a civilian president. Oligui has since leveraged Gabon’s role as the world’s fourth-largest producer of manganese – a critical component in steelmaking and EV batteries – to drive greater local processing, by instituting a manganese ore export ban. The Trump administration was also likely eager to strengthen maritime security cooperation with Gabon and counter Chinese plans for a naval base in the region. Beijing has held commercial interests in Port Gentil – Gabon’s oil and gas hub – since 2014. To address the city’s isolation from the rest of Gabon and normalise sea routes into the port, Chinese state-owned firms constructed a 95km road linking Port Gentil to Omboué at a cost of USD 663 million. While the Bongo administration was close to China, allowing rumours of a Port Gentil naval base to swirl, Oligui has assumed a position of strategic ambiguity concerning the base.

With the Trump administration intent on bilateral deal-making, and tensions with China set to continue, further African states may well find themselves similarly empowered in 2026. Kenya is well positioned to step up, having narrowly missed out on a visit by US Vice-President JD Vance in November, but having secured a consolation prize engagement with US Secretary of State Marco Rubio. Angola is another potential candidate, with President João Lourenço having invested heavily in Washington lobbyists to offset its historically strong connection to China.

Climate change and the energy transition

3. Climate stasis continues, while forests gain ground

Last year, we warned that revenue mobilisation would be slow towards the New Collective Quantified Goal (NCQG) – a target agreed in 2024 to provide developing countries with at least USD 300 million of climate finance from public sources per year by 2035. Indeed, while states affirmed their commitment to the NCQG and began optimising the deployment of funds at COP30 this November, progress has been incremental. Commitments were similarly weak on the protection of tropical forests, despite this being a major focus for the Brazilian hosts.

Developing countries were not able to achieve their main aim of gaining greater clarity from governments in the Global North about the level of funding they intend to allocate towards the NCQG. This agenda item was not opened at COP30, with developed nations sticking with a vague commitment to “take the lead” on mobilising the USD 300 billion per year NCQG funds by 2035. Furthermore, the Baku to Belém roadmap to USD 1.3 trillion – a joint effort between COP29 hosts Azerbaijan and COP30 hosts Brazil to chart a path towards consensual levels of climate finance – was merely “noted” at the Belém summit. The roadmap was made public a week before COP30 began and it was written in an opaque manner. There appears to be limited appetite to further engage with the roadmap among key stakeholders, although Brazil has pledged to hold further consultations surrounding its contents. There was some progress on the NCQG, however. This included a high-level ministerial dialogue at the summit, and the establishment of a two-year work programme to inform the implementation and delivery of the funds. Crucially, it was agreed that there would be efforts to triple adaptation finance by 2035 under the NCQG. Addressing the outsized role of climate mitigation vis-a-vis adaptation was a major focus at COP30, a position taken by the African Group of Negotiators after aligning on their strategy at the Africa Climate Summit in Addis Ababa in September. African stakeholders will keep pushing for a strong focus towards adaptation finance in 2026.

Held in the Amazonian city of Belém, COP30 had been dubbed the “Forest COP”, with global leaders setting the stage for the launch of the Tropical Forest Forever Facility (TFFF). This mechanism is designed to incentivise the conservation and expansion of tropical forests by paying countries in the tropics to maintain existing forests. This marks a major break with the traditional model of carbon credits, which operate on the concept of “additionality”, with value derived from protecting forests in imminent danger of destruction. The TFFF should be a boon for high forest, low deforestation countries like Gabon and the Republic of Congo which have, to date, struggled to generate major financial gains from their vast forest cover. However, funding was in short supply, with the initial USD 5.5 billion in commitments falling well below the USD 25 billion targeted by the Brazilian hosts. Nevertheless, Africa stands to benefit from a separate scheme, the Belém Call for the Forests of the Congo Basin, which was unveiled the same day, and intends to mobilise USD 2.5 billion over five years to stop deforestation in Central Africa.

Vague commitments in 2025 indicate that climate finance mobilisation is unlikely to keep pace with the ambitious targets set out in the NCQG in 2026. However, the launch of the TFFF sets up Gabon and the Republic of Congo for a promising 2026, with the prospect of locking in large-scale and long-term financing to keep forests standing at COP31 in Antalya, Türkiye. This would strengthen the hands of the African Group of Negotiators ahead of COP32 in Addis Ababa, Ethiopia in 2027.

4. The EU identifies carrots to accompany climate regulation sticks

Last year, we warned that Africa’s more industrialised economies would need to prepare for compliance with the EU’s flagship climate initiative, the Carbon Border Adjustment Mechanism (CBAM), which will become operational in January 2026. At COP30 in Brazil, delegates from beyond the bloc took aim at CBAM, which China, India and Japan labelled CBAM as “unilateral and arbitrary”, while Saudi Arabia sought to characterise it as an “economic transfer from the poor to the rich, disguised as climate action”.

The EU’s carbon emissions pricing regime continues to weigh heavily on South Africa, the continent’s most industrialised economy. With its heavy reliance on coal-based energy, exports such as steel, aluminium, and automotive components are particularly vulnerable. Even before the regulations come into effect, the cash-strapped government has come under pressure to subsidise loss-making industry, after ArcelorMittal South Africa (AMSA) announced plans to close two of its biggest steel mills in the country, barring state support. AMSA has failed to reach a deal with the Industrial Development Corporation (IDC), hastening an end to long steel production in South Africa. However, Pretoria has been seeking to leverage its strong ties to Brussels to develop new future-facing industries. In March 2025, the European Commission launched its first Clean Trade and Investment Partnership (CTIP) with South Africa, promising investment, skills and technology, and developing strategic industries along the clean energy supply chain. The CTIP promises to boost European investment in the critical minerals value chain, from exploration to recycling, and battery production. This is likely to entail a major focus on Platinum Group Metals (PGMs), which are integral to South Africa’s emerging hydrogen economy, and manganese, which is essential to steelmaking and is an important input in electric vehicle (EV) batteries. Astutely, the EU finalised the CTIP and allied clean energy cooperation agreements with South Africa in the lead up to the G20 Summit in Johannesburg last month. This included a strategic partnership on sustainable minerals and metals value chains, funding for green hydrogen and batteries, backed by a Global Gateway investment package worth EUR 4.7 billion, and pledges around Scaling Up Renewables in Africa.

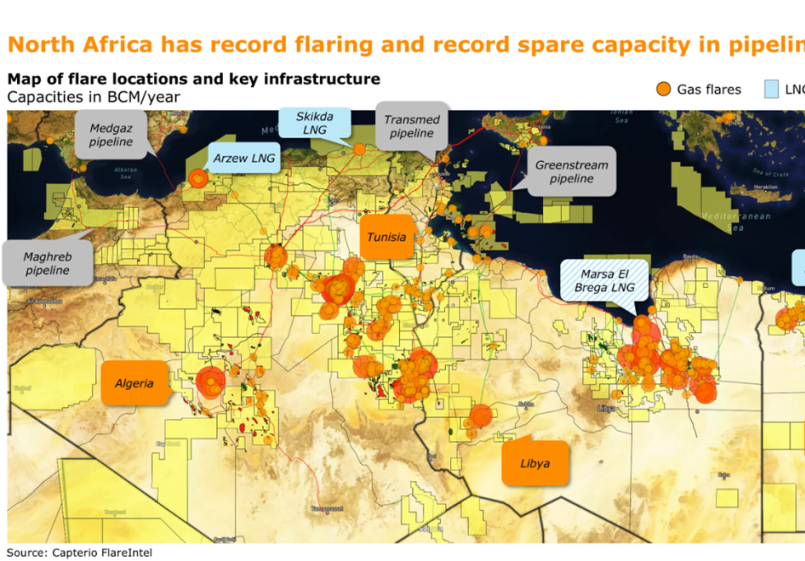

Fortunately, European decision-makers are increasingly aware of the need to combine a clean energy carrot with a legal stick, as evidenced with international partners’ efforts to build support for the EU Methane Regulation. This measure aims to halt the avoidable release of methane into the atmosphere, both in Europe and global supply chains, and is backed by major LNG importers Japan and South Korea. The regulation is driving growing scrutiny of upstream operations, including in key African suppliers of oil and gas, such as Algeria, Libya, Nigeria and Angola. International partners are increasingly working with African national oil companies to strengthen methane measurement, monitoring, reporting and verification (MMRV) regimes, and reduce emissions through mandatory leak detection and repair (LDAR) campaigns. Data collection is also ramping up, as the EU prepares a methane transparency database, which is set to be launched in February 2026. This will be followed by the publication of methane performance profiles for producers, importers and third countries from August 2026. Recognising the need to alleviate the burden, the EU is making efforts to fund methane action and bolster clean energy cooperation across affected markets. Emerging tools include the EUR 175 million pilot scheme “You Collect, We Buy”, which was initially trialed in Algeria and is now being explored in Egypt. Other promising mechanisms include the EU-backed Methane Abatement Partnership Roadmap, the World Bank’s Global Flaring and Methane Reduction trust fund, and Japan and South Korea’s CLEAN project.

In the year ahead, we expect more African governments to recognise the three-fold benefits of action on methane, in terms of broadening energy access, strengthening public finances and tackling climate goals simultaneously. While more work remains to be done to ensure that African national oil companies and European importers have the requisite measures in place to comply with the Methane Regulation, we expect the EU’s carrot and stick approach can galvanise action in 2026. Africa Practice and our partners Environmental Defense Fund will continue to facilitate strategic dialogue between policy-makers, financial institutions and industry stakeholders across the continent in the year ahead.

5. Gulf investors continue mineral acquisition spree, with Qatar opening its piggy bank

Last year, we predicted an increase in deals between Africa’s mineral rich states and partners from the Gulf, highlighting the emergence of Saudi Arabia’s Manara Minerals and the UAE’s International Resources Holding (IRH). This trend has continued over the last year, with further high-profile investments in critical mineral supply chains, and the emergence of a new influential player from Qatar.

In June 2025, IRH acquired a majority stake in Alphamin Resources’ Bisie tin complex in the Democratic Republic of the Congo (DRC). This demonstrated the Emirates’ ability to quickly deploy capital in risky jurisdictions, keeping key assets running and – critically for Western allies, such as the US – out of Chinese hands. IRH is overseen by Sheikh Tahnoon bin Zayed Al Nahyan, a member of the Abu Dhabi royal family, who also serves as the UAE’s national security adviser. IRH is no stranger to Africa, having entered Zambia with the acquisition of a 51% stake in Mopani Copper Mines from state mining company ZCCM Investments Holdings in 2024. Manara Minerals – a joint venture between the Saudi Public Investment Fund and state mining company Ma’aden – also has its eyes on the Congolese and Zambian copperbelts, as well as assets in Botswana and Namibia. Saudi Arabia has pledged to invest USD 10 billion in African mining projects; however, unlike IRH, Manara is focused on the acquisition of minority stakes in copper, nickel, lithium and iron ore projects. Qatar has even bigger ambitions still, after Al Mansour Holding pledged to invest an eye-watering USD 21 billion in the DRC, in an apparent attempt to galvanise the Doha-brokered DRC-Rwanda peace deal. This came on top of an earlier commitment by the firm’s owner Sheikh Mansour Al Thani to invest USD 70 billion across Botswana, Mozambique, Zambia and Zimbabwe during a 10-day tour of Southern Africa.

Such efforts will need to take account of growing regional aspirations around value addition to critical minerals. Under South Africa’s Presidency, the G20 adopted a critical minerals framework with a major emphasis on value addition in the Global South, encouraging nations to move up the value chain through beneficiation, refining, and processing. South African Minister of Mineral and Petroleum Resources Gwede Mantashe went further, calling for regional governments and African institutions to work together on processing, in order to strengthen the continent’s collective bargaining power. Naturally, Mantashe regards South Africa as “well placed to lead a continental response”, presumably oblivious to fear that Pretoria will dominate any cross-border collaboration. Such grandiose ambitions are at odds with research from the Natural Resource Governance Institute (NRGI), which indicates that small, targeted coalitions focused on specific value chain opportunities are most likely to succeed, while efforts to grow African mineral value chains hinge on the distribution of benefits to all participating countries. Fears that one side will miss out lie behind the fracturing of a putative DRC-Zambia cross-border special economic zone for the production of battery precursors, which has now splintered into plans to establish two separate zones, undermining economies of scale and the benefits of collaboration. 2026 promises to serve as a test for regional collaboration in an entirely different commodity, with the race to secure control of diamond giant De Beers. Botswana initially trumpeted its ambitions to secure a controlling stake in the firm, with President Duma Boko presenting this as “a matter of economic sovereignty.” Angolan state miner Endiama subsequently entered the race, proposing a pan-African consortium of diamond producing nations to jointly run the company.

Angola’s ability to convince Botswana, Namibia and South Africa to join forces promises will serve as a major test for regional cross-border collaboration in 2026. In the meantime, we expect Emirati, Saudi and Qatari firms to continue to snap up strategic African mining assets.

Geoeconomics

6. US protectionism prompts Africa to revisit regional trade ties and look to Europe

Last year, we warned that Africa would remain vulnerable to externalities, including an impending American pivot towards protectionism, which threatens the future of the African Growth and Opportunity Act (AGOA). Alas our prediction was correct, and continental economies are still dealing with the fall-out.

Trump’s “Liberation Day” tariffs hit leading beneficiaries of AGOA hard, signalling the end to 25 years of America granting preferential trade terms to Africa. Lesotho was hit with a 50% reciprocal tariff on account of dubious calculations, which divided America’s trade deficit with a foreign country by that country’s total exports to the US. AGOA – which had been pivotal in building up Lesotho’s nascent clothing manufacturing industry – became its Achilles’ heel. The landlocked nation, which had become the continent’s second-largest apparel exporter, with around 75% of all exports heading to the US, found its textile industry decimated overnight. The move put 35,000 jobs at risk and upended a sector which had contributed around 15% of GDP. While the Trump administration subsequently revisited its tariffs, the failure to renew AGOA has imposed a major toll on other export-dependent nations, including Madagascar and Kenya. Nairobi missed out on a crucial opportunity to sweet-talk Vice-President JD Vance when he cancelled a planned visit in November 2025. However, Kenya continues to pursue trade talks with the US, eschewing a Strategic Trade and Investment Partnership (STIP) proposed by the Biden administration that was focused on removing non-tariff barriers (NTBs) in favour of a new bilateral trade agreement with the Trump administration. President William Ruto engaged US Secretary of State Marco Rubio in Washington DC in early December to move negotiations forward, complaining that industries like textiles, agriculture, pharmaceuticals and digital services were being stymied by the 10% tariff imposed by Trump earlier in 2025. In 2026, Kenya will continue to push for a preferential deal with the US to offset the uncertainty over its EU-Economic Partnership Agreement, which entered into force in 2024, after the East Africa Court of Justice has moved to suspend the pact over a suit contesting its compatibility with the common market established under the East African Community.

Meanwhile, other African nations unable to count on such global trade access will increasingly look East. Capitalising on the backlash against Trump’s tariffs, in June 2025 China announced a zero-tariff policy granting duty-free access to all 53 African countries with which it maintains diplomatic relations. Although China was already importing 97-98% of tariff lines from 33 African LDCs, trade was dominated by raw materials, including crude oil, iron ore, copper, cobalt, and other minerals. The move promises to pave the way for African nations to export value-added goods to China (assuming they can compete on price with the workshop of the world). In the interim, we expect African economies to prioritise agricultural exports, working with China to trade through dedicated “green lanes”, which now exist for a range of commodities, including avocados, coffee, chillies, cashews, and sesame seeds.

While political machinations and the US government shutdown killed off plans to renew AGOA ahead of its expiry in September, at the time of publication, the House of Representatives was due to consider a bill to extend the initiative to December 2028. In the event this proposal stalls, African states will need to fall back on Trump’s transactional approach to trade diplomacy, while South Africa is unlikely to make any headway.

7. South Africa’s G20 Presidency drives international financial architecture reform

Last year, we predicted that Africa would continue to contend with elevated borrowing costs, while calls for reform of the international financial architecture grew louder. Indeed, it was a busy year for African finance ministers and central bankers, with sovereigns regaining access to global markets on more favourable terms, and Pretoria shaping the outlook for the G20 Common Framework.

In March, South African Finance Minister Enoch Godongwana launched an Africa expert panel to tackle the continental debt crisis, as part of South Africa’s G20 Presidency. More than half of Africa’s 1.3 billion people live in countries that commit more to debt interest payments than on social expenditure such as health, education, and infrastructure, according to National Treasury calculations. Former South African Finance Minister Trevor Manuel took up responsibility for chairing the panel, working with the continent’s leading economists, bankers, think tankers and academics to prepare a high-level report, and building on input from the Business 20 (B20). His findings, launched at the G20 summit in Johannesburg, included important recommendations for tackling the mounting debt crisis. It reaffirmed the G20’s commitment to assisting low- and middle-income countries address debt vulnerabilities, pledging stronger, more predictable implementation of the Common Framework. Building on our earlier efforts to promote greater nuance and cut the cost of capital on the continent, Africa Practice is supporting these initiatives, and the priorities of the B20 Finance & Infrastructure Task Force, through the Financing Africa Forward coalition. Over the year ahead, Africa Practice and our partners, the ONE Campaign and the Africa Finance Corporation, will be advancing the Financing Africa Forward Blueprint for Action, which was adopted as a B20 Legacy Initiative. The blueprint lays out 11 steps focused on strengthening creditworthiness through better data and analytics, modernising the international financial architecture, and reducing structural biases in sovereign risk assessment.

Efforts to renew the global financial architecture become urgent this year, as evidenced by Ghana and Zambia’s debt restructuring process under the Common Framework. The Paris Club of Western lenders pushed Accra and Lusaka to restructure the commercial debt owed to the Eastern and Southern African Trade and Development Bank (TDB) and African Export–Import Bank before finalising their exit from sovereign default status – flying the in face of claims by TDB and Afreximbank that they benefit from preferred creditor status, which conventionally exempts creditors from participating in debt restructurings that typically involve losses. This status is traditionally afforded to concessional lenders like the World Bank and IMF to safeguard their AAA credit ratings and ensure they provide low-cost credit, not lenders which issue commercial debt at higher interest rates and do not benefit from comparable high credit ratings.

Senegal is also grappling with the inequities of international financial architecture. The country is increasingly at risk of defaulting on its debts after the Court of Auditors unearthed some USD 8 billion of hidden liabilities incurred by the previous administration. The IMF validated concerns that President Macky Sall’s government misreported economic data to secure more favourable credit terms from international lenders, noting a “conscious decision to underestimate the debt stock” from 2019 to 2024. This has left the new government with a budget deficit equal to 14% of GDP and public debt exceeding 130% of GDP. President Bassirou Diomaye Faye is faced with having to atone for the sins of his predecessor, as the IMF has suspended a USD 1.8 billion lending package and called for Senegal to restructure its public debt. Prime Minister Ousmane Sonko rejected this proposal, stressing fiscal sovereignty and warning that such a move would damage investor confidence and restrict access to international markets. While divisions between the two men make predictions hazardous, barring a U-turn by the government, rapid debt restructuring and renewed IMF lending, sovereign default appears increasingly likely.

In the year ahead, African sovereigns will be hopeful that such fiscal chicanery and attempts to conceal borrowing will become a thing of the past. The launch of the Africa Credit Rating Agency (AfCRA) in 2026 provides a route to address the perception bias that unfairly paints continental governments as unreliable debtors, thereby driving up borrowing costs. AfCRA, as an AU-backed but privately-owned entity, will help to broaden perspectives of continental creditworthiness. Its initial focus will be on rating local currency debt – an area which typically receives scant attention from global credit ratings agencies, but which offers a route to stimulate domestic capital markets and reduce foreign currency risk on the continent. AfCRA is also breaking the mould when it comes to decision-making, and has committed to transparent governance structures which enable greater scrutiny of its methodology.

Elections and democracy

8. Sham elections in Uganda and Ethiopia erode government legitimacy

As we predicted, 2025 served as a low-water mark for African democracy, with incumbents re-elected in questionable circumstances. In Côte d’Ivoire, demonstrations by supporters of ineligible candidates Laurent Gbagbo and Tidjane Thiam hung over a vote which returned President Alassane Ouattara to a fourth term. In Tanzania, the jailing of Chadema leader Tundu Lissu and exclusion of ACT candidate Luhaga Mpina enabled the “coronation” of President Samia Suluhu Hassan, but at the cost of an unprecedented wave of violence. Finally, in Gabon, General Brice Oligui Nguema secured election as a civilian president, barely two years after the coup that brought him to power. Africa’s democratic credentials are unlikely to be burnished by polls scheduled for Uganda and Ethiopia in the year ahead.

Uganda goes to the polls in January 2026, with a vote that is highly likely to prolong the rule of President Yoweri Museveni, who has been in power since 1986 and is (at least) 81 years old. Museveni’s chief rival is the 43-year old singer Robert Kyagulani – better known as Bobi Wine – whose primary support base is young voters. Museveni has defeated Kyagulani in previous elections by a wide margin, but votes have been marred by irregularities and intimidation by security forces. In May, Museveni’s son Muhoozi Kainerugaba, who also serves as Uganda’s military chief, admitted that he was holding opposition activist Eddie Mutwe in his basement and threatened that Bobi Wine would “be next.”

Ethiopia’s elections are set to be similarly undemocratic, despite Prime Minister Abiy Ahmed’s attempts to present the June 2026 polls as the country’s “best” to date. However, we fear that the ballot is shaping up to be a turbulent replay of the flawed 2021 process, this time with higher stakes and yet more instability. Ethiopia is grappling with three fundamental issues that leave it ill-prepared to hold a credible, national vote. First, a worsening security crisis – with Tigray, Amhara, Oromia and Somali regions all suffering from instability – means that the state risks replicating the flawed process of 2021, but on a much larger scale. Second, the National Election Board of Ethiopia (NEBE) faces a crisis of both logistics and legitimacy. Despite its shortcomings in 2021, the electoral body is targeting digital registration of polling stations and a technology-based voter and candidate registration platform, turning a blind eye to realities on the ground. Finally, an acute cost-of-living crisis and the frustration of perceived state neglect hang over the process, with a long-promised national dialogue yet to materialise.

The year ahead may well represent another low-water mark for African democracy, barring more competitive ballots in Zambia and Cabo Verde, São Tomé and Príncipe, Benin and The Gambia. Either way, ballots in Uganda and Ethiopia appear to be a foregone conclusion, along with the Republic of Congo and Djibouti, where long-serving presidents are bound to extend their rule.

9. Sahelian pariahs and Guinea find new bedfellows in Madagascar and Bissau

Last year, we reflected on military regimes in Francophone West Africa, predicting that the Sahelian juntas of Burkina Faso, Mali and Niger would formally break ties with the Economic Community of West African States (ECOWAS) and deepen their integration under the Confederation of Sahel States (CES). The trio went further, introducing a common travel passport, establishing a 5,000-strong regional security force to tackle instability in the Sahel, and quitting the International Criminal Court (ICC). We also highlighted the risk that the Guinean military regime would proceed with a constitutional referendum and transitional elections based on an outdated voters’ roll. That plebiscite took place in September, strengthening the hand of General Mamady Doumbouya, who is now set to secure election as head of state in a flawed vote on 28 December. Yet, as we look ahead to 2026, our attention turns to two more coup-affected states.

In Madagascar, President Andry Rajoelina was forced to dissolve the government in late September following youth-led demonstrations over electricity outages and water shortages. The protests resulted in dozens of fatalities, with a heavy-handed police response drawing condemnation from the UN High Commissioner for Human Rights. Rajoelina fled the country in early October, leaving elite military unit CAPSAT to seize power, with the lower house of parliament voting to impeach the embattled statesman. Ironically, this is the very same military unit that helped Rajoelina ascend to power in a 2009 coup that overthrew former President Marc Ravalomanana. CAPSAT’s Colonel Michael Randrianirina is now Madagascar’s interim leader, under a two-year transition period. He is targeting elections within 15–18 months, following a national consultation and constitutional referendum. The transition timeline has helped Madagascar to win acceptance from the Southern African Development Community (SADC), African Union, France, and intriguingly, Russia. However, the Gen-Z protest movement that toppled Rajoelina appears to be losing influence, amid internal divisions. In 2026, we expect youth activists to return to the streets, as the junta struggles to resolve grievances and Gen-Z senses the extent of their exclusion from the transition process, which is falling under the patronage of more established civil society groups, such as the Council of Christian Churches in Madagascar (FFKM).

While pressure from the street proved decisive in Madagascar, the forces behind Guinea-Bissau’s November coup d’état are much more shadowy. The putsch came just as election results were due to be released, and was publicised by President Umaro Sissoco Embaló, indicating he may have stage-managed the incident. Sissoco Embaló claimed to have been arrested by the Head of the Casa Militar at the Presidency, Brigadier General Dinis Incanha. The “deposed” president had been governing by decree since December 2023, when he leveraged a supposed attempted coup to dissolve the legislature, conveniently sidelining his main rival Domingos Simões Pereira of the African Party for the Independence of Guinea and Cape Verde (PAIGC). While Sissoco Embaló is now in exile, Senegalese Prime Minister Ousmane Sonko and former Nigerian president Goodluck Jonathan have both suggested the coup may have been staged. Whatever the truth, General Horta N’Tam is now Guinea-Bissau’s new interim leader, having been installed by coup-leader Brigadier General Incanha. The duo and their junta, the High Military Command for the Restoration of National Security and Public Order (ACMRSNOP), is promising a one-year transition, and has named Ilídio Vieira Té – an ally of Sissoco Embaló – as prime minister. ECOWAS has appointed Sierra Leonean President Julius Maada Bio (himself a former putschist) as lead negotiator, and regional heads of state are set to meet for an emergency session on Guinea-Bissau on 14 December. However, any efforts are unlikely to unseat the generals, given ECOWAS’ weakened stance following the departure of the Sahelian states, and Maada Bio’s poor track-record as lead negotiator with the Guinean junta. Instead, Bissau will likely follow Conakry’s lead, promising ambitious reforms, but allowing deadlines to slip, making fresh elections unlikely before 2027. This could be a risky strategy for Guinea-Bissau – a country with few foreign allies and deep ties to narcotraffickers – at a time of heightened US interest in countering the international drugs trade.

With democracy on the ropes, the outlook for the year ahead remains bleak. With francophone Africa at the vanguard of “coup-tagion” over the past few years, we cannot rule out a putsch in the anglophone sphere in 2026. South Sudan’s President Salva Kiir is rumoured to be in ill-health, the operation of oil pipelines crucial for exports are at the mercy of security developments in war-torn Sudan, and the president has increasingly concentrated power around his family members after dismissing the rich and powerful Vice President Bol Mel in November.

Security

10. Conflicts in Sudan and DRC continue to fester, despite international pressure

Last year, we provided a grim outlook for Sudan, fearing that international mediation would falter and that foreign military cooperation would determine the direction of the conflict. Alas, there is still no clear end in sight for Sudan’s civil war, which has lasted nearly three years.

The myriad of external actors implicated in the conflict face little international pressure to halt support for the Rapid Support Forces (RSF) or the Sudanese Armed Forces (SAF). Since the war began, more than 12 million people have been displaced, around half of the population is experiencing acute food insecurity – with many living under famine conditions, and conservative estimates count the death toll at over 150,000. Around 4 million Sudanese refugees have fled overseas, most of which have sought safety in neighbouring countries, including Egypt, Chad and South Sudan, with Libya, Ethiopia, Uganda, and the Central African Republic. The two key military developments of 2025 were the SAF’s victory in the Battle of Khartoum and the RSF’s seizure of El Fasher, which has led to each of the belligerent parties consolidating control in distinct regions of Sudan, with competing administrations. The RSF has established itself in Nyala, the South Darfur capital, while the SAF is situated in Port Sudan, the capital of Red Sea State. While both sides have been accused of human rights violations, the SAF benefits from greater international legitimacy, with the RSF accused of carrying out widespread war crimes, especially in the Darfur region of Sudan. When El Fasher was seized, evidence of mass killings were visible from satellite imagery.

In 2026, we expect an intensification of the conflict in Kordofan – situated between RSF-controlled Darfur and the SAF-controlled east. The region has experienced an uptick of drone strikes and troop deployments since November. At the time of publication, the RSF captured the garrison town of Babnusa, and looked to be pressing on towards the major mercantile city of El Obeid, some 250 miles from the capital, Khartoum. While we expect the US to continue its efforts to bring the war to an end, under the auspices of the Quad – comprising the US and Saudi Arabia, as well as key backers of the warring parties (UAE and Egypt) – but we see little hope for the roadmap for peace published in November. The plan culminates with a nine-month political transition to a civilian-led government, the disbandment of the RSF, and the removal of Islamist elements from the SAF. Unsurprisingly, the parties to the conflict oppose a plan that proposes to weaken their authority.

Meanwhile, hopes for peace in Eastern Congo have ebbed and flowed over the last year, with Qatari- and American-backed peace processes. While DRC and Rwanda signed a US-brokered deal in the presence of President Trump on 4 December, the ceremony itself underscored tensions, with Congolese President Félix Tshisekedi and Rwandan President Paul Kagame avoiding eye contact and declining to shake hands during the event. Barely a day had passed before the recriminations began, with Tshisekedi accusing Kagame of breaching the Washington Accord, heightening doubts over the extent of shared commitment to cease hostilities. While Rwanda dismissed Congolese accusations as “ridiculous”, the M23 militia it controls continues to operate on the ground.

Irrespective of American muscle or Qatari mediation, the hopes for sustained peace in Eastern Congo remain bleak in 2026.

Proud to be BCorp. We are part of the global movement for an inclusive, equitable, and regenerative economic system. Learn more