We are excited to announce that Brink is now part of Africa Practice. Learn more

Letter on Africa: Cutting methane can ease Africa’s energy crunch

The continent has an immediate opportunity to make the most of its energy resources by capturing gas that is currently slipping away.

As global gas markets tightened in March, a tanker carrying LNG from Nigeria to France abruptly changed course towards Asia. The diversion was a small but telling signal of a larger reality: supply is constrained, competition is intensifying and every available cargo is being pulled towards the highest bidder.

At the same time, vast volumes of African gas are going to waste.

Methane that is routinely leaked, flared or vented into the atmosphere across the continent is both wasteful and damaging because methane is a powerful climate pollutant. But methane emissions are also a market failure. Unlike carbon dioxide, methane is not a useless energy byproduct—it is the product. Every tonne emitted is energy that could be used domestically or sold abroad as natural gas.

At a moment of global disruption, that distinction matters. The war in the Middle East has disrupted roughly 20% of global oil and gas flows, tightening LNG supply chains and pushing prices higher. Yet this same moment presents a clear opportunity. By reducing methane emissions and gas flaring, African producers can increase supply, generate revenue and strengthen energy security without waiting years for new projects to come online.

The scale of the opportunity is substantial. According to the IEA, Africa’s energy sector emitted an estimated 17mt of methane in 2025. Every cubic metre released into the atmosphere is gas that could otherwise power homes, support industry or be exported at a premium in today’s market, leveraging Africa’s underutilised gas export capacity.

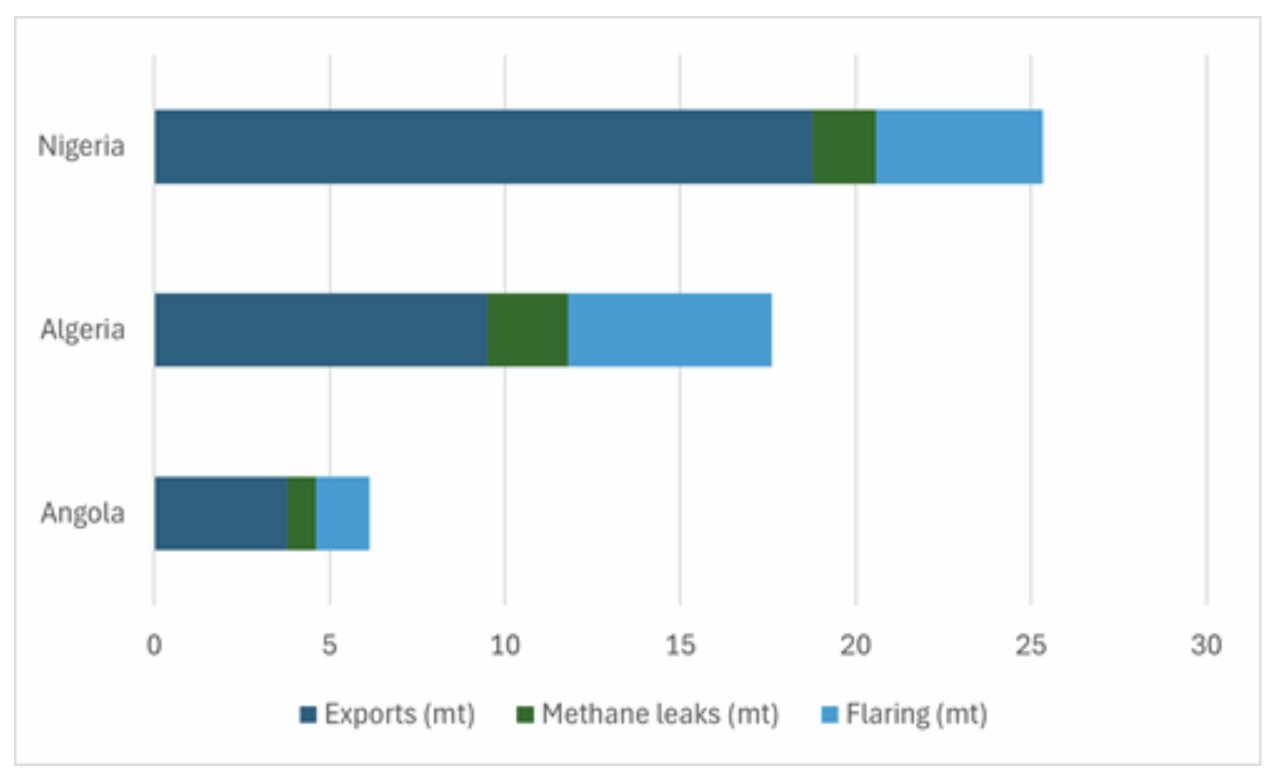

The continent can export nearly 80mt/yr of LNG, yet many facilities operate well below capacity due to upstream supply constraints. In Algeria, LNG exports in 2025 reached just 9.5mt, according to the Middle East Economic Survey, less than half of its installed capacity of 25.3mt/yr, as per Group of Liquefied Natural Gas Importers data. Even in Nigeria, where LNG facilities run closer to full capacity, methane leaks and infrastructure challenges continue to limit supply.

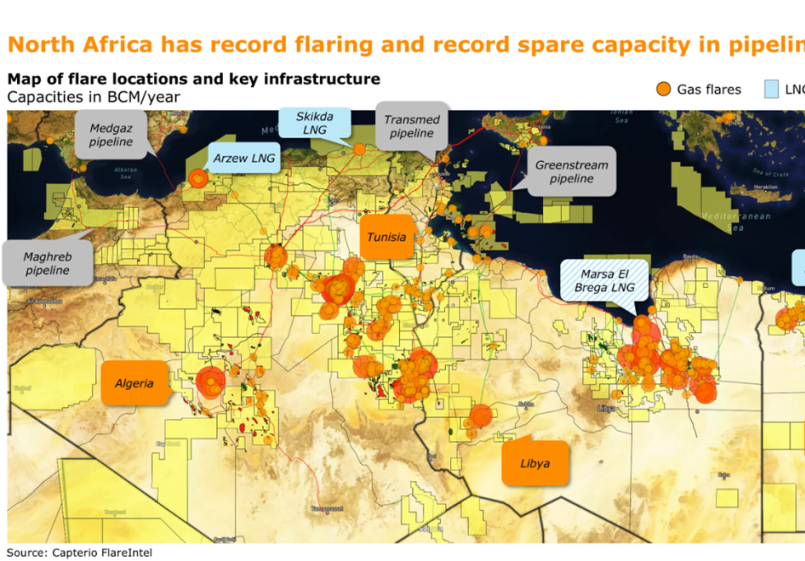

Capturing this gas offers a rare alignment of economic, energy and climate priorities. In North Africa alone, Algeria, Libya and Egypt lose an estimated 21bcm/yr of gas through flaring and leakage, according to calculations by Capterio. This is equivalent to around 14% of their production and up to $6b in lost annual revenue. Much of this waste can be addressed using proven technologies, often at low or even negative cost once the value of captured gas is considered.

Leading the way

There are already examples of progress. Angola LNG has shown that gas that would otherwise be flared can be captured and commercialised at scale. In Algeria, flare gas recovery projects and partnerships with international operators are beginning to unlock similar value. Nigeria LNG has achieved high standards of methane measurement and reporting, demonstrating what is possible across a broader system.

This shift in attitudes towards methane is being reinforced by the world’s largest gas buyers. The EU’s Methane Regulation will introduce stricter requirements on measurement and reporting, with compliance expected in the next few years. At the same time, major LNG buyers, including Japan and South Korea, are backing initiatives that favour suppliers able to demonstrate credible methane reductions.

For African exporters, this is both a risk and an opportunity. Those who act early can secure access to premium markets and strengthen long-term demand. Those that do not risk being sidelined as emissions performance becomes a differentiator.

Importantly, African governments and NOCs are not starting from zero. Many are already engaged in initiatives such as the Oil and Gas Methane Partnership 2.0, which provides a framework for measuring and managing emissions. Others have committed to ending routine flaring and reducing methane under international pledges.

The challenge now is execution—which means focusing on practical steps that can deliver results quickly. Identifying high-emission assets, deploying leak detection and repair, investing in flare gas recovery and strengthening infrastructure to keep gas in the system. It also means mobilising financing, which is increasingly accessible as better data reduces risk and improves project bankability.

International partners and technical experts are ready to support these efforts. But leadership will need to come from within.

At a time when global supply is tight and prices are elevated, the value of every molecule of gas has increased. For Africa, the methane opportunity is immediate. The gas is already there, so the question is whether it will be captured or continue to slip away.

This article was first published in Petroleum Economist

Related articles

Proud to be BCorp. We are part of the global movement for an inclusive, equitable, and regenerative economic system. Learn more