We are excited to announce that Brink is now part of Africa Practice. Learn more

Europe’s untapped gas opportunity: North Africa’s USD 6 billion flares

War in the Middle East, disruptions to Qatari LNG flows and even an exploding Russian LNG tanker have again exposed the fragility of Europe’s gas security. Price volatility and bidding wars between Asia and Europe are now inevitable. With gas price futures today above EUR64/MWh (USD 22 per mmbtu), and storage (at 29%, almost a record low), Europe could be heading to a crisis deeper than in 2022. For now, US and Russian exporters are cashing in.

Yet just south of Europe, three major exporters – Algeria, Egypt and Libya – lose more than 20 bcm of gas each year through flaring, venting and leaks. Europe and its North African partners therefore share a clear strategic opportunity: monetising this wasted gas.

Three factors now align. First, European gas markets are seeking a broader base of reliable supply that meets their upcoming import standards. Second, existing export infrastructure – four pipelines and four LNG terminals – operates at one-third utilisation, leaving significant spare capacity. Third, exporting countries are eager to deploy proven commercial solutions, increase export revenues, reduce emissions and improve competitiveness.

Now is the moment for leadership and commitment on both sides of the Mediterranean. By capturing wasted gas, Europe can diversify its supply and strengthen energy security, North Africa can generate around USD 6 billion in additional export revenues, and the planet benefits from lower CO₂ and methane emissions.

North Africa’s gas opportunity

The three gas giants of North Africa – Algeria, Libya and Egypt, which produce 3.8% of global gas supply – carry unrealised potential due to widespread gas flaring (combusted associated gas from oil production), methane leakage and venting. Together, these losses total 21 bcm per year (14% of their gas production) and represent a revenue opportunity of up to USD 6 billion annually (assuming a conservative USD 7.5/MMBtu) that also lowers emissions and improves export competitiveness.

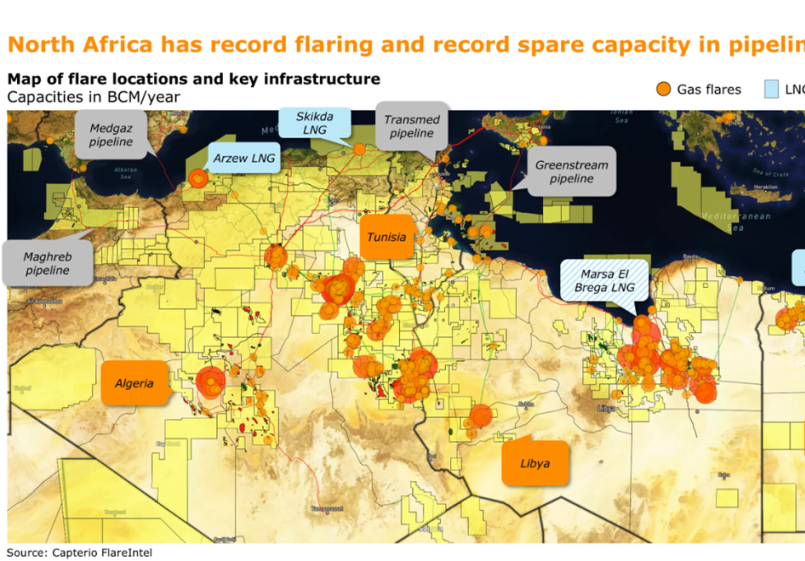

Data from Capterio’s FlareIntel, which track every flare every day, highlights the scale of the opportunity (see Figure below).

Figure 1: Overview of gas flaring in North Africa, highlighting the location of flares and their proximity to existing major gas exporting infrastructure. Source: Capterio FlareIntel.

The Table below shows how all three countries exhibit high levels of routine flaring (and for some, record highs), despite commitments to eliminate it by 2030 and elevated flaring intensities.

Table: Scale of the emissions opportunity North Africa’s exporting countries. Source: Capterio FlareIntel (for 2025 flaring data) IEA (for 2024 methane data) and EIA (2025 production data).

A key enabler of gas capture is North Africa’s deep integration with European gas markets. Europe is connected via four pipelines from Algeria and Libya and four LNG terminals in Egypt and Algeria. As Europe seeks to finally wean itself off Russian gas, and potentially diversify away from US LNG, looking across the Mediterranean for additional supply is an obvious step.

North Africa’s challenging domestic backdrop

Each country faces significant challenges: rising domestic demand and ageing oil and gas fields are driving declining gas exports. Total exports from Algeria, Libya and Egypt in 2025 were 41 bcm, down 33% from 2021 (with piped gas falling 16% and LNG by 56%), leading to record-low utilisation rates of 34% (see Figure). In 2025, Algeria accounted for 96% of exports. Algeria is now Italy’s primary gas supplier (substituting Russia) and Spain’s second-largest gas supplier.

Figure 2: Gas exports from Libya, Egypt and Algeria via pipeline (grey) and LNG (orange). Combined spare capacity (white, dotted) is at a record high. 2026 figures shown as annualised based on data to 25 February. Source: EU; Kpler; Capterio analysis.

If exports are at record lows and capacity is underutilised, why are record volumes of exportable gas still being flared? At a time of fiscal pressure, pending methane regulation and rising electricity demand, this paradox must become a policy priority.

Governments have three options to boost exports. First, they could increase domestic gas production, supported by renewed international interest, as the bid rounds in Libya and Algeria attest. Second, they could scale-up renewables and improve energy efficiency, to lower domestic consumption and free gas for export. Third, they could capture wasted gas.

Of these, tackling gas flaring (and associated methane) is likely the quickest win. Unlike exploration, these volumes are already on production and avoid long-lead infrastructure. Capturing waste delivers near-term supply without locking in assets or conflicting with long-term transition goals.

How to solve gas flaring?

Flare capture is often portrayed as technically complex or economically marginal. Yet Capterio’s data and project analyses suggest otherwise, as does the IEA. Capture projects should also be viewed in the context of existing supply pressures. Declining production has forced Egypt to import expensive LNG. Libya pays export prices to secure gas and liquid fuels for power generation.

Practical solutions are already emerging. In Libya, repairs to legacy compression equipment have helped reduce upset flaring in some oil fields. Plans are afoot to install compressors to transport flared gas through existing underused trunklines. Algeria has been exploring better ways to use processing plants and pipelines by improving coordination across its joint ventures. In Egypt, projects that capture flared gas for power generation have helped displace liquid fuels, saving costs and lowering emissions.

Capitalising on the growing sense of urgency

The timing is critical. The European Union’s Methane Regulation will impose stringent monitoring, reporting and performance standards on imported gas from 2030. Exporters with elevated methane intensities risk competitive disadvantage, reputational damage or restricted market access.

The EU and international oil companies have an imperative to partner with North African governments, national oil companies and regulators to advance gas capture and clean energy cooperation. Delivering this will require leadership, coordination, credible data, regulatory enforcement, capital mobilisation and political will. The EU already has multiple tools at its disposal.

A revamp of the proposed “You Collect, We Buy” scheme that targeted Algeria and Egypt, could commit capital to gas capture schemes across the region. Brussels could lean on the Euromajors to assume greater responsibility for flaring, venting and fugitive emissions at their non-operated joint ventures. Finally, the EU should pursue a win-win, leveraging the Trans-Mediterranean Renewable Energy and Clean-Tech Cooperation Initiative (T-MED) to decarbonise electricity generation, and free up gas for export.

In an era of energy security concerns and tightening methane rules, reducing flaring, venting and leaks in North Africa is more than an environmental obligation. It is a strategic opportunity that strengthens European supply resilience, supports exporting economies and accelerates decarbonisation.

This is an abridged version of an article co-authored by Mark Davis, CEO of Capterio, and Nick Branson, Lead Advisor at Africa Practice.

Proud to be BCorp. We are part of the global movement for an inclusive, equitable, and regenerative economic system. Learn more