We are excited to announce that Brink is now part of Africa Practice. Learn more

The new rules of African gold

Africa’s gold sector is entering a new phase. Record prices have strengthened investor appetite for African deposits, but they have also hardened governments’ determination to retain more value at home. Gold is no longer treated simply as a taxable export commodity. Across key jurisdictions, it is an increasingly strategic asset: a source of fiscal revenue, foreign exchange, domestic industrialisation, central-bank reserves and political legitimacy.

Beyond fiscal policy to support national development priorities

This is the core of the current shift: state value capture. African governments are moving beyond royalties and corporate tax toward tools designed to control more of the value in the gold value chain. For investors, the implication is direct. Project success will depend not only on geology, capital and execution, but on the ability to align with national priorities, demonstrate local value creation and build durable political legitimacy.

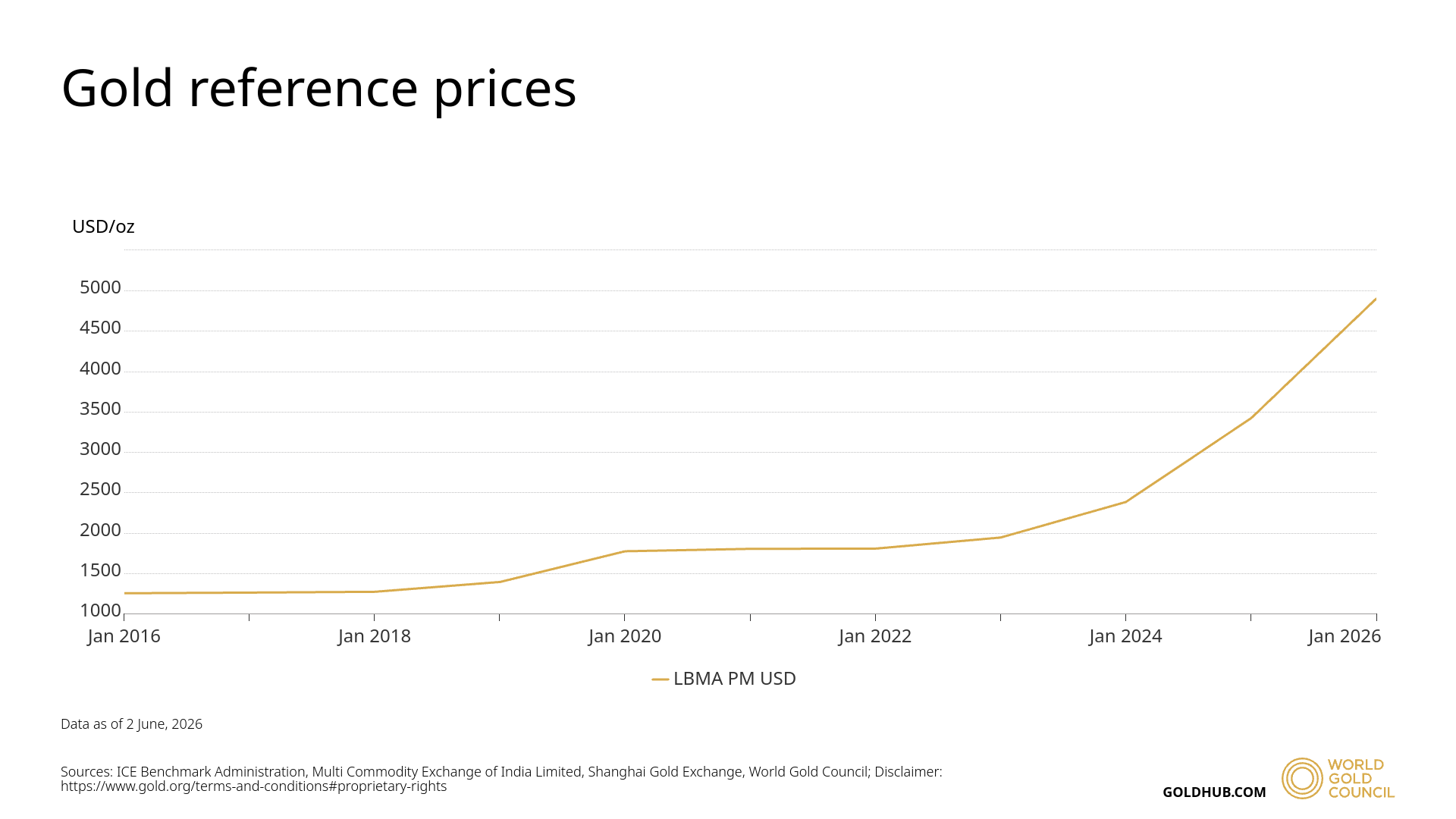

For mining companies, sustained high prices have improved project economics and intensified competition for exploration ground. According to S&P Global’s World Exploration Trends, gold remained the world’s leading exploration target in 2025, with US$6.15bn allocated globally. For governments, this price environment creates a different imperative: if gold is generating exceptional value, more of that value must remain in-country. This does not mean rejecting foreign investment. It means redefining the contract between capital and the state.

That shift reflects a longstanding African policy ambition. The Africa Mining Vision, adopted in 2009, calls for mining to move beyond enclave extraction and support structural transformation through stronger governance, domestic linkages, beneficiation, skills transfer and better use of resource rents. Gold is now becoming one of its clearest test cases.

The question for governments is no longer only how much tax a mine pays. It is whether the project advances national priorities: local content, domestic processing, skills development, formalisation of artisanal mining, foreign-exchange retention and strategic state participation. States want influence over the value chain itself: who buys gold, who exports it, where it is refined, how foreign exchange is retained and how public institutions gain direct exposure to the asset.

The new mechanisms for state value capture

The new gold-regulation agenda is borrowing from some of the instincts long familiar in oil and gas. Mining is increasingly adopting much of the same sovereign value-capture logic: stronger state participation, domestic value retention, export and forex controls, local-content obligations and more active oversight of project structures.

The mechanisms vary by country, but the direction is consistent. Governments are recalibrating royalties and taxes, narrowing stability protections, increasing discretion over licence renewals, creating gold boards, expanding central-bank purchase programmes, tightening forex repatriation, and formalising artisanal and small-scale mining. Together, these tools mark a shift from fiscal collection to strategic control.

Artisanal mining is central to this agenda. In its 2026 study On the Trail of African Gold, SWISSAID found that more than one tonne of undeclared gold leaves Africa every day. For governments, this is not only a compliance problem – it represents a loss of tax revenue, foreign exchange, traceability and sovereign control over a vital strategic resource.

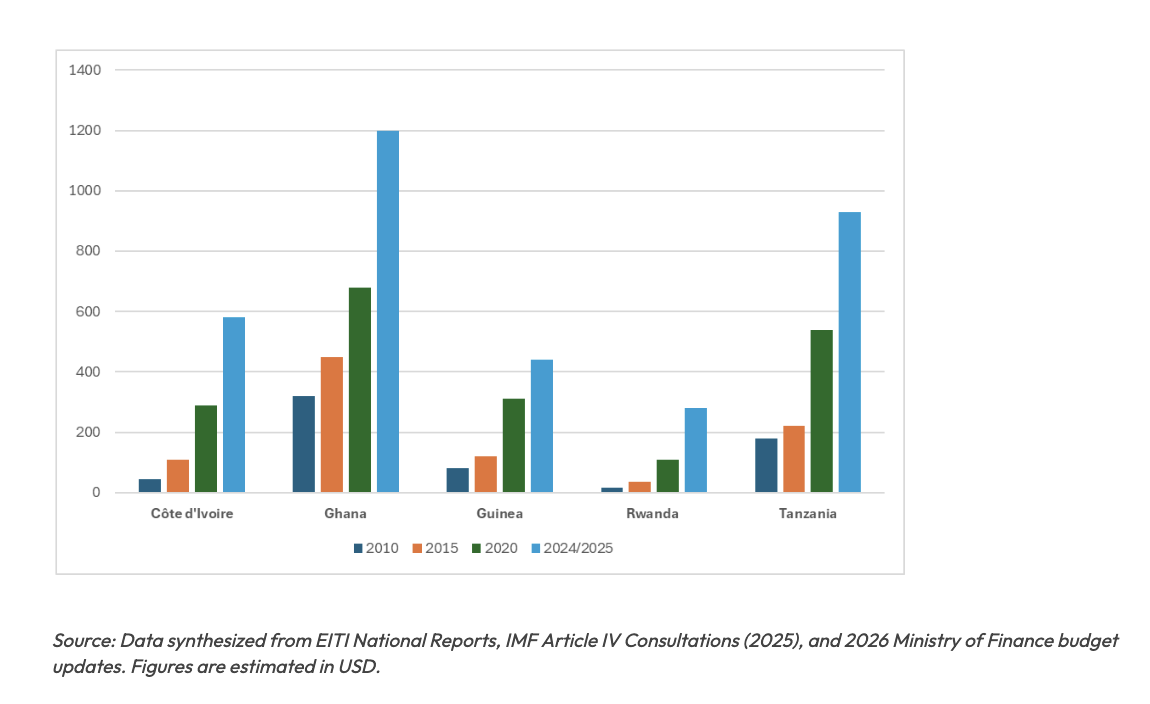

Across Côte d’Ivoire, Ghana, Guinea, Rwanda and Tanzania, the same trend is producing different state responses.

Côte d’Ivoire represents calibrated value capture. Its 8% royalty increases the fiscal burden on gold producers, but the country continues to protect its reputation for stability and administrative support. Its partnership-based approach to artisanal mining formalisation points to traceability and professionalisation, rather than exclusion.

Ghana is a more aggressive reformer. Its policy direction combines stronger fiscal value capture, tighter control of gold trading, domestic value-chain ambitions and reduced tolerance for automatic contractual protections. Ghana’s GoldBod matters because it turns the state into a direct actor in the gold market, with exclusive authority over licensed small-scale gold.

Guinea is using a sophisticated approach combining enforcement and state partnerships. Licence repossessions and exploration-permit cancellations signalled that dormant or non-compliant ground would no longer be tolerated. The Resolute Mining / Nimba Mining Company MoU points to the next phase: the state positioning itself as a co-creator of future gold projects.

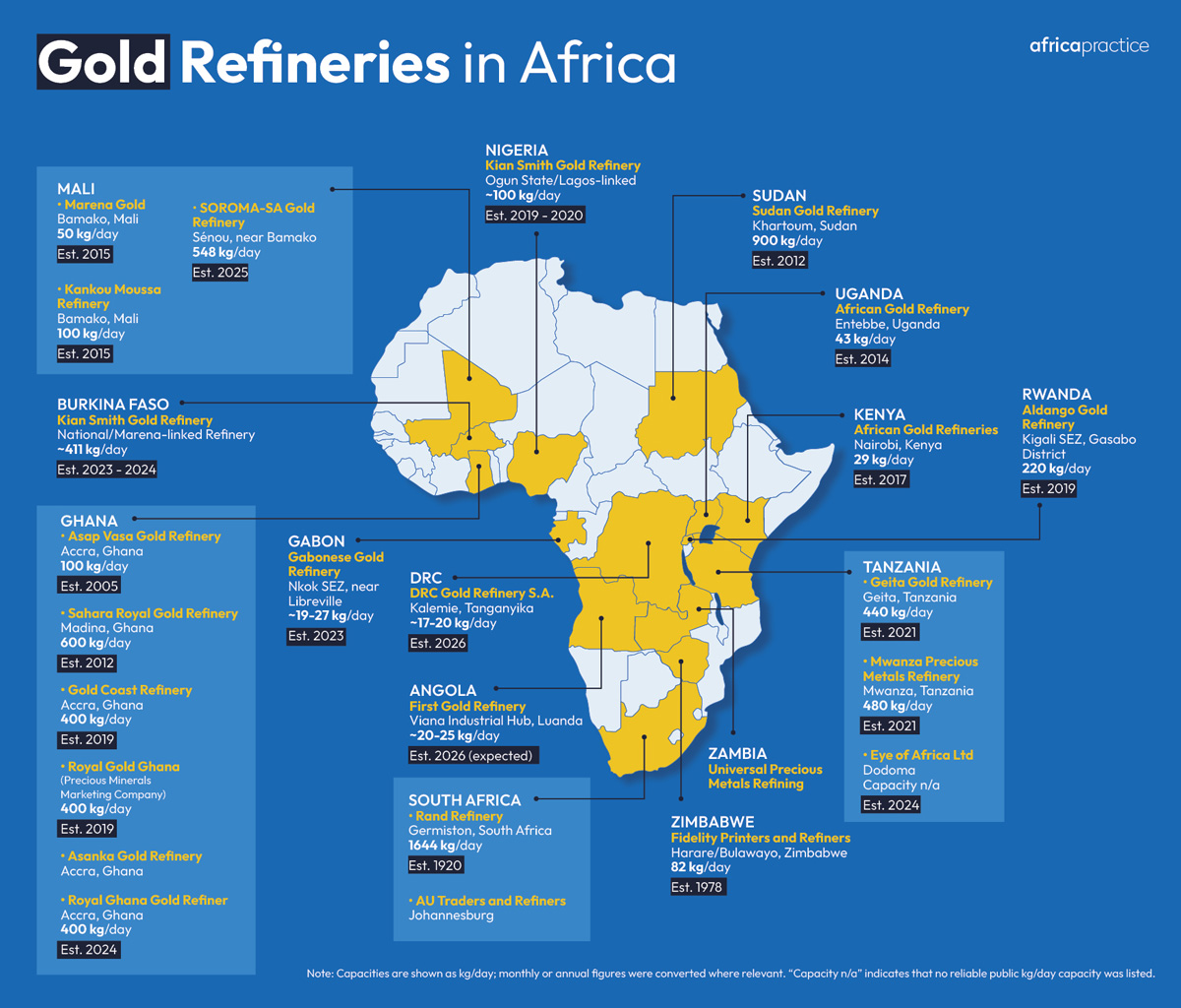

Rwanda combines formalisation with refining-led control. The 2024 Mining Law confirms state ownership of minerals and centralises regulation through the Rwanda Mines, Petroleum and Gas Board. The 2024 Minerals Tax Law cuts gold royalty and export taxes to 0.5% to encourage formal sales, while domestic refining is promoted through the Gasabo Gold Refinery.

Tanzania is building a domestic value-addition model. Its central-bank gold purchasing mechanism, refining incentives and protection of small-scale mining for nationals connect mining policy with reserve accumulation, local processing and economic sovereignty.

Evolution of estimated fiscal revenue (royalties + corporate taxes) directly attributed to the gold sector, in million USD

Investors should learn to navigate a new landscape

Africa’s gold sector is entering an era of strategic regulation. Investors can no longer assess jurisdictions through their mining codes alone. The real investment environment now includes fiscal predictability, state behaviour, forex exposure, licence-renewal risk, domestic-processing requirements, ASM policy, local-content enforcement and the quality of government engagement.

Operators will need to demonstrate alignment with national development plans, credible local procurement, transparent fiscal contributions, skills transfer and realistic domestic value-addition strategies. The premium is shifting toward companies that can build political legitimacy alongside technical and financial capability.

The new rules of African gold are therefore clear. Governments still want investment, but on terms that deliver more visible national value. For miners, the winners will be those that understand regulation not as a compliance exercise, but as a strategic negotiation over sovereignty, development and trust.

Related articles

Proud to be BCorp. We are part of the global movement for an inclusive, equitable, and regenerative economic system. Learn more